August 1, 2024

By Anne Dabbs,

NCAN TN Support Group Leader, NET Patient

and

Tom Wilson,

NCAN WI Support Group Leader, NET Advocate

Since 2006, Medicare enrollees have had the opportunity to participate in Medicare Part D which is the coverage available for prescription drug costs. Participation in Medicare Part D is available to Original Medicare participants and those who purchase Medicare Advantage Plans. The coverage and administration of Medicare Part D plans has been a work in progress since its inception.

Starting in 2025, Medicare Part D will see significant additional changes aimed at reducing out-of-pocket costs for beneficiaries, thanks to provisions in the Inflation Reduction Act. These changes include a new out-of-pocket spending cap, elimination of the coverage gap phase, increased cost-sharing responsibilities for Part D plans and drug manufacturers, and the introduction of monthly payment options for out-of-pocket costs.

There are six key Medicare reforms which were passed in 2022 as part of the Inflation Reduction Act (IRA). Some of these changes went into effect in 2023, several more in 2024, and the final ones will take effect in 2025.

2025 Medicare Changes:

1. $2,000 Out-of-Pocket Cap:

• Beginning in 2025, Medicare Part D will cap out-of-pocket drug costs at $2,000 per year. This cap will be indexed to rise annually based on per capita Part D costs. This change is particularly beneficial for patients with high medication costs, such as those with neuroendocrine cancer who often require expensive treatments (KFF) (MedicareFAQ).

• This $2,000 cap is an exceptionally beneficial change for those of us with multiple expensive drugs for our Neuroendocrine Cancer and other ailments. These changes will eliminate the “donut hole” experienced by many. A basic example of the changes which have occurred in part due to the Inflation Reduction Act is as follows:

2023 – Here is an example of one of our NETs drugs – Everolimus or Afinitor. The cost of Everolimus (Afinitor) is approximately $18,167 per month or $218,004 annually. The NETs patient out of pocket responsibility was $10,484 in 2023 which included costs through the various Part D stages leading up to the catastrophic stage where they paid 5%. If other drugs were taken (i.e. Xermelo) this would be additive. Much of the out-of-pocket expense was paid in the first month or two, a very heavy burden to the patient.

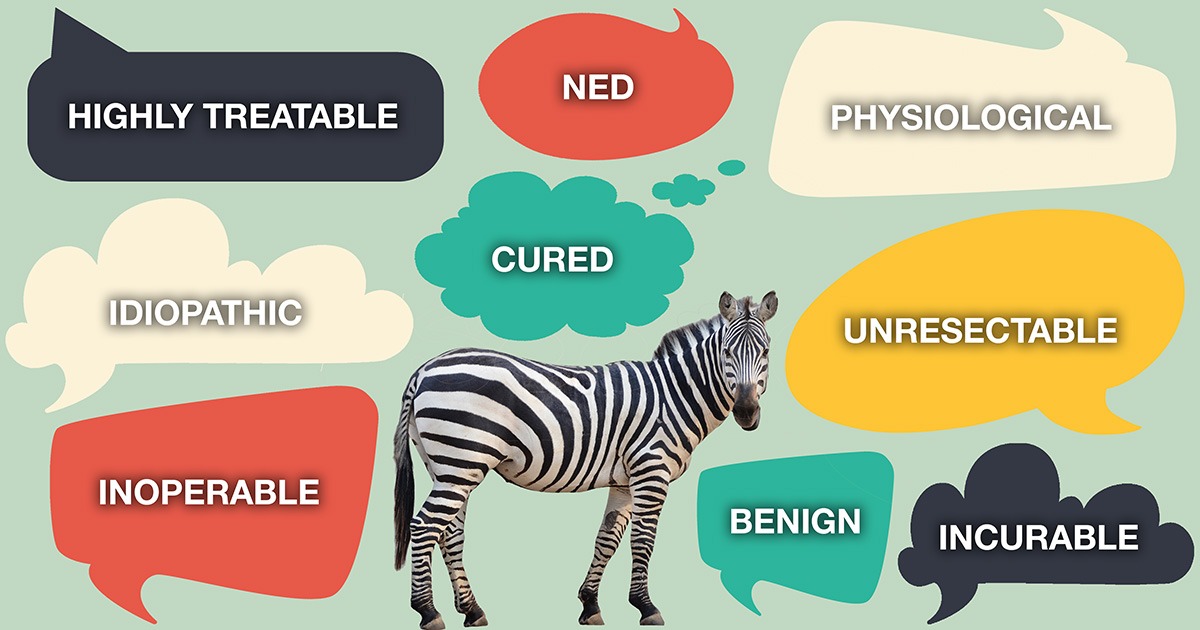

• In 2024, the maximum out of pocket dropped to about $3,300. This was usually all or mostly paid in the first month or two of the year, an onerous amount in the beginning of the year. In the Everolimus (Afinitor) example above, a patient would save $7,184 just on this one drug.

• In 2025, the maximum out of pocket will decline to $2,000. This would be for any drugs a NETs patient might take such as Everolimus, Xermelo, Creon, etc. The changes in 2024 and 2025 will save thousands of dollars for NETs patients who take these high-cost drugs.

2. Elimination of the Coverage Gap (Donut Hole):

• The coverage gap, where beneficiaries previously paid a larger share of drug costs after a certain spending threshold, will be eliminated. This ensures continuous coverage and more predictable costs throughout the year (MedicareFAQ).

3. Cost-Sharing Adjustments in Catastrophic Phase:

• In the catastrophic phase, the share of costs covered by Part D plans will increase, and Medicare’s share will decrease. Drug manufacturers will also be required to offer price discounts in this phase, further reducing costs for beneficiaries (KFF) (Medicare Rights Center).

4. Monthly Out-of-Pocket Payments:

• For the first time, beneficiaries will have the option to spread their out-of-pocket costs into capped monthly payments, making it easier to manage and budget for prescription drug expenses (MedicareFAQ) . This is similar to the leveling of charges for natural gas or electricity. This may be referred to as “cost smoothing” or “MP3” in the marketplace.

Impact on Neuroendocrine Cancer Patients:

Patients with neuroendocrine cancer often face high costs for their medications. The new $2,000 out-of-pocket cap will significantly reduce their financial burden, as these patients can quickly reach the catastrophic coverage phase due to the high cost of cancer treatments. The elimination of the coverage gap ensures that these patients will not experience a sudden increase in drug costs during the year. Additionally, the ability to spread out payments will help patients better manage their finances (KFF) (Medicare Rights Center).

Government agencies which oversee Medicare Programs have made publications available which fully explain the additional reforms beginning January 2025. In September 2024, existing Medicare enrollees will receive their Annual Notice of Changes (ANOC) from their Plan administrators which will include these new benefits among other considerations. Newcomers to Medicare will find the appropriate information in the office US government Medicare handbook “Medicare & You 2025” which is mailed to prospective enrollees several months prior to their 65th birthday.

Individuals with chronic illnesses will especially benefit from becoming educated about Medicare and the Medigap Supplemental Plans. Every state has free resources available to enrollees to help you better understand your options.

To connect with qualified Medicare experts before you begin your search for an insurance company you can:

• Visit the Medicare.gov website to start a virtual chat.

• Call the 1-800-Medicare support line (800-633-4227).

• Reach out to a counselor at your State health Insurance Assistance program (SHIP) whose link is found on your state’s dot gov website.

• Find a licensed Medicare enrollment specialist through the national Council of Aging.

5. Important Reminders as You Consider Your Medicare Coverage Choices:

1) Medigap plans (mostly frequently named by letters such as Plan G or Plan K) are standardized, but not all plans are offered in every state. Not all insurance companies may sell policies for a particular plan in your state.

2) Compare the benefits of each lettered plan available in your state to help you find the one that best meets your needs now and potentially in your future. With a chronic condition like NETs, you will most likely not be able to switch Medigap providers so choose wisely.

3) Once you have selected the Plan you feel is best for your needs, talk to other insurance companies which sell the standardized plan in your state.

4) Call your State Insurance Department for a list of companies selling policies in your state. Be sure to ask if they have any complaints registered against those companies.

5) Your local State Health Insurance Assistance Program (SHIP) is not connected to any insurance company or health plan and can provide free consulting to help you determine which company offers the best selection and pricing to meet your needs. The benefits in each lettered plan are identical regardless of which insurance company you consult. Price is the only difference between the same lettered Plan policies sold by different companies.

The changes to Medicare Part D in 2025 represent a major shift towards more affordable and predictable drug costs for beneficiaries. For patients with Neuroendocrine Cancer, these changes offer substantial financial relief and improved access to necessary treatments. Beneficiaries should review their current plans and consider these new options to optimize their coverage and reduce their out-of-pocket expenses.

If you need support, NCAN is here for you. Don’t hesitate to reach out if you need us.

* The above information was compiled by using the following links and helpful resources for better understanding Medicare. The information contained here is not a specific recommendation for any choice for any patient. Our recommendation is to avail yourself of comparisons and expectations for the best Medicare program for your individual needs.

Helpful Resources:

GOVERNMENT SITES:

Medicare.gov

CMS.gov (centers for Medicare and Medicaid Services)

HHS.gov (health and human services)

Healthcare.gov

USA.gov

Shiphelp.org

COMMERCIAL AND ADVOCACY WEBSITES AND VIDEOS:

Medicareinteracive.com

Kkf.org/medicare

Boomerbenefits.com

Gohealth.com

Healthline.com

Nasi.org

Medigap vs. Medicare Advantage | Which Is Best for You in 2024?

Comparing Advantage VS Supplemental COST on $200k Hospital Stay

Ranking The BEST Supplemental Plans For 2024!

WARNING: Why I Would NEVER Choose An Advantage Plan for 2024!

Hospitals Are Dropping Medicare Advantage Plans

Recent Comments